Alt Lending week ending September 10th 2021

Overseas companies find British red tape a hindrance to doing business.

I am not a great fan of the FCA and think they should perhaps take a leaf out of the medical professions book when nudging UK banks in one direction or another. “First do no harm” comes to mind. I have known for some time that it can be very difficult for businesses to open a bank account in the UK. In fact in some cases it is probably easier to open a bank than open a bank account? It seems that overseas companies wishing to conduct business in the UK are being turned down on compliance grounds for what would seem to be arbitrary, petty and bureaucratic reasons. This is not helpful for global Britain or for anything else I suspect, just part of a mindless conduit of poor and under qualified staff over sensitive regulation, untrained staff and a lack of sanction against those who enforce rules in which are sometimes not even rules in the first place. In most businesses client acquisition is critical to survival yet some of our banks turn away business as if it is part of their remit. Perhaps the business prevention department does actually exist.

The social implications of low interest rates.

The Harvard based National Bureau of economic research has recently produced a paper which takes a close look at the relationship between plentiful credit supply and equality. It argues that this factor is even more important than the lack of housing supply which continually blights the UK. It also points out that cheap and plentiful credit is only available to those who are the best credit risks and the rest of the punters , particularly those who don’t have and cannot aspire to be property owners and those who have fallen foul of credit agencies because of previous misdemeanours just get poorer at the expense of those who are already richer. Is this what Boris Johnson calls levelling up? I don’t think so. My own view is that this is politically unacceptable and that a lot more power should flow back to individuals to right wrongs or misconceptions. Credit should be assessed at the time the application is made not on historical data that might now not be relevant. Unfortunately technology is very good at managing quantitative data but not so good at qualitative stuff. Don’t expect any changes soon. Our credit markets are arbitrary and unfair and, shamefully, are designed to be so.

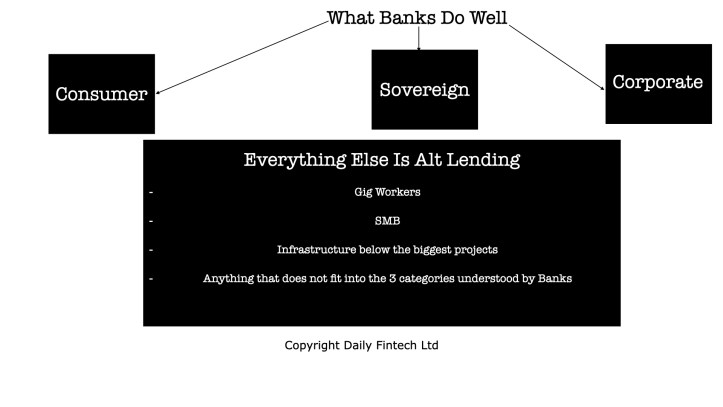

Killing off the Zombies is essential

Following on from the point made above Matthew Lynn in the Daily Telegraph makes the very valid point that the dead wood in the form of zombie companies that are only surviving because of ultra low interest rates combined with government handouts during the pandemic should shuffle off their mortal coil much quicker in order to help the economy. The banking system has a role to play in this. Companies that have no future except on life support don’t really do anyone very good but as the banking systems principal source of revenue is interest differential and government meddling and excessive regulation restrict the ability to trade profitable banks no longer have the cushion necessary to cover the write offs required. On top of this most zombies could do with a really good shake up, something the banks used to be pretty good at enforcing. However as the banks no longer train bankers in the critical skills of helping firms progress through leverage so the skill of recognising how to help those struggling companies has also atrophied. All rather sad, as it doesn’t do anyone any good at all.

Howard Tolman is a well-known banker, technologist and entrepreneur in London,

We have a self imposed constraint of 3 news stories per week because we serve busy senior Fintech leaders who just want succinct and important information.For context on Alt Lending please read the Interview with Howard Tolman about the future of Alt Lending and read articles tagged Alt Lending in our archives.

Daily Fintech’s original insight is made available to you for US$143 a year (which equates to $2.75 per week). $2.75 buys you a coffee (maybe), or the cost of a week’s subscription to the global Fintech blog – caffeine for the mind that could be worth $ millions.